This knowledge is brought to you by Venkat Krishnan, just one of the thousands of top management consultants on Expert360. Sign up free to hire freelancers here, or apply to become an Expert360 consultant here.

Table of Contents

- The Telco Market Across Australia, New Zealand and Singapore

- Why Telcos Are Becoming Customer Centric: Problems With The Traditional Model

- How Leading Large Telcos Are Putting The Customer First

- Turning The Customer Care Model Upside Down

- The Future Of Telco Customer Centricity

- Infographic

This article aims to explore the changing face of customer experience in the Telco industry in the Asia Pacific region, referencing Australia, New Zealand and Singapore markets. With revenue pressures on telcos from increasing competitive intensity, regulatory pressures and the rolling out of the government regulated National Broadband Network, telcos are trying to find fresh ways to innovate and differentiate themselves. Most leading telcos are aiming to differentiate from one another through customer centric strategies. This highlights the critical nature of customer experience and the importance of customer segmentation in the telecom industry. This article will focus in depth on the above key factors that are affecting telco revenues (competitive intensity, regulatory pressures and the rolling out of the government regulated National Broadband Network). Furthermore this article explores how various telcos are increasing their customer focus by rebranding themselves and changing the way they look at customer experience by channel including retail, call centres and digital. The report is written based on secondary research and the author's first-hand knowledge in the industry and has a strong focus on the Australian telco market.

The Telco Market Across Australia, New Zealand and Singapore

Australia, New Zealand and Singapore while portraying varying degrees of cultural differences, are alike in the way the telco industry has developed in these countries. In all three countries, telcos owe their growth to Government backed companies, namely Telstra in Australia, Singtel in Singapore and Spark (previously Telecom NZ) in New Zealand. This government backed start has led to all three telcos currently holding significant market shares in their respective geographies.

Fixed & Mobile Revenue Markets in Australia

Increasing Competitive Intensity In Mobile And Fixed Markets

In Singapore, TPG won the right to be the 4th mobile telco operator in December 2016. Similarly, TPG is poised to build its own mobile network in Australia after its $1.2B 4G mobile spectrum splurge. TPG already has close to 2 million customers on its fixed network in Australia, which it intends to successfully leverage to bring new competition to the mobile market. The government backed rollout of NBN (National Broadband Network) also referred to as UFB (Ultra-Fast Broadband) in NZ is another factor driving increased competitiveness in the APAC telco industry. Traditionally, the fixed line copper and HFC (Hybrid Fibre coaxial) networks were held by the likes of Telstra, Singtel and Spark. Other providers had to lease the lines from these providers to supply broadband to the customers. With NBN, government backed entities hold control of the network infrastructure thereby giving access to even smaller players to resell NBN and breaking the near monopolies of Telstra, Singtel and Spark. This has led to a raft of new players coming into the market including mobile only players venturing into the fixed market (e.g. Vodafone in Australia). New technologies disrupting the telco industry in unfathomable ways globally. SMS revenues formed a significant portion of telco revenues ($2 per SMS sent in 2010) until the advent of messaging apps like WhatsApp and Messenger. Overnight, the telco industry saw its SMS revenues wiped out as customers turned to these messaging platforms. Similarly, calling revenues has suffered as data usage gains more prominence and consumers are increasingly using video calling over Skype and similar platforms. Soon telcos will struggle to monetise calls at all, as the shift becomes more permanent to over the top (OTT) platforms.

Data Is The Latest Revenue Frontier For Telcos

Recent trends are putting pressure on the way even data gets monetised by telcos. With companies like Jio in India and Sprint in US throwing away data revenue with “Free unlimited data for 1 year” offers, it is not far that companies like TPG will follow suit with similar offers in Singapore and Australia in a bid to gain market share. Players like Sigfox and Lora are starting to play in unlicensed spectrum. This is not impacting the current telco revenues, but it is impacting the future opportunities for telcos in the Internet of Things space.

Government Regulations Putting Pressure On Telco Revenues

In Australia, the Mobile Termination Access Service rates (MTAS rates) are regulated by the government. We have seen a decline in the MTAS rates over the years. MTAS is essentially the fee that a telco operator gets by landing the call/SMS from another operator to a customer on its own network. With reduction in MTAS rates, Mobile network operators (MNOs) are struggling to justify the investments they have made on mobile infrastructure.

The impact of all the above factors is two-fold: 1. For consumers, mobile and fixed services are becoming increasingly cheaper 2. The telco industry revenues and margins are under immense pressure and MNOs are losing their stronghold due to increasing competition, technological disruptions and NBN as lines are blurred between traditional MNOs and new entrants. The only way going forward for telcos to differentiate themselves from each other is through improving their customer experience strategy.

Why Telcos Are Becoming Customer Centric: Problems With The Traditional Model

The traditional telco model has been to sell fixed and mobile services to mass market customers and businesses. The demands from customers were simple and for telcos it was a matter of selling the most number of services to customers and ensuring that their network was robust enough to not cause any customer complaints leading to churn. The focus was on: 1. Investing in and building a high-quality network and blocking competition out with heavy investments in spectrum and network build 2. Huge advertisement and promotional spend to reach the masses and create awareness 3. Having a large enough retail presence to reach of customers in their neighbourhood 4. Having a large telesales and customer care staff to sell and handle queries. However the winds have changed. Customers are becoming network agnostic as NBN has taken network off the table. New players and the digital age have brought in smarter players who spend a fraction of the traditional media spend on online channels and yet have a profound marketing impact. Many new age telco retailers do not have any retail points of presence but thrive with their online entity and digital self-service models. This means that traditional telcos are finding it hard to manage their cost base while offering competitively priced products for their customers. The traditional telco business models are no longer viable and focusing on customer centricity for large corporates is becoming increasingly essential.

How Leading Large Telcos Are Putting The Customer First

As telcos come under pressure and lose their competitive advantages, many telcos are looking at alternate options.

1. Rebranding As Digital Entities

A classic example is Telstra. As Telstra’s revenues face headwinds, the oldest Australian telco is rebranding itself as a “Technology” company. Telstra customers can now ask the company for tech advice that relates not only to their home broadband or phone line, but can also ask to troubleshoot their computer or mobile issues. As the number of connected devices in home expected to at least double by 2020, this is a huge opportunity for a telco to be the go to entity to solve all customer related tech issues. In a similar fashion, Optus is rebranding itself as a Mobile and Fixed commodity provider to a Mobile led Entertainment company

2. Increasing Product Portfolio

Most telcos are going beyond offering fixed and mobile services to offering content. Telstra owns a 50% stake in Foxtel. Optus surprised the market by snatching the rights to stream English Premier League football in Australia. Similarly, in New Zealand, Vodafone sell Sky TV bundled packages. Telstra has made a foray into the health sector a few years ago and provides services ranging from managing databases to tele-health. It excels in providing mobility tools that give doctors and patients greater flexibility, and secure, centralised data storage.

Singtel is making leading strides in the Internet of Things sector with its development of the Smart Cities network in collaboration with the Singapore government. Bundling other products into the core mobile and fixed offerings means that customers have a one stop shop for their entertainment, health and internet of things needs. It helps them buy these services from a trusted provider and reduce the cost of these services.

3. Changes in channels

Operators risk being caught unprepared and losing control of the customer relationship to more digitally savvy players. Today’s sales and service strategy relies largely on siloed channels and emphasises physical retail and traditional call centres. The online experience will improve customer service in telecoms (especially in service) but has a long way to go to match the optimal digital experiences consumers have come to expect (like Amazon, Netflix, and Uber). Telecoms can no longer use old models to serve new customers. Those unprepared to change risk irreparable harm to their businesses. Consumers desire an omni-channel experience; however, they also demand an integrated experience in which information flows seamlessly. Operators need a forward-thinking strategy if they expect to maintain and strengthen their customer relationships.

Making Physical Stores Smart

As consumer behaviour continues to shop in physical retail stores, but increasingly in combination with a digital channel, many Network operators with retail stores are trying to make their physical stores smart. Telstra’s George Street store in Sydney is a case to be reckoned with when it comes to customer experience. From the moment you step inside, you see an environment that’s built around the customer. It’s warm, inviting and open. Every part of the customer’s experience has been personalised with interactive new technologies that enable a customer to discover the richness of Telstra’s communication solutions. A favourite is the “Sandbox” of the Device Lab, where a customer can place different handsets on an interactive table that provides popup information comparing features, pricing and even independent online reviews. All of this can be saved up in a ‘Tap and Take’ card which has a personalised code the customer can use to log in and retrieve information online after he or she has left the store. However, as the purpose of retail stores changes from being sales driven to showcase driven, telecoms are constantly rationalising their store footprint to reduce costs.

Using Digital To Enhance The Online And Advisory Experience

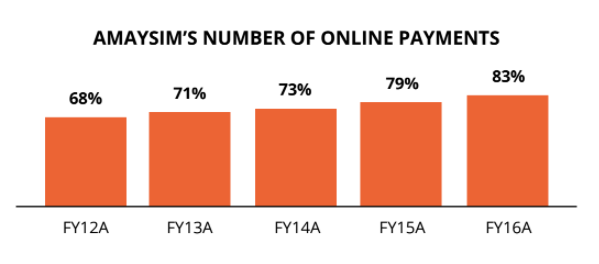

There is a rapid shift in the way customers have taken up to doing everything online. In fact, many virtual network operators have an online only business model. E.g. Amaysim’s business model as below. (Source: Amaysim Financial disclosures Jun-16)

Amaysim claims that the percentage of customers paying online has increased significantly from 68% in 2012 to 83% in 2016.

Equally, Amaysim’s number of customers who activated online has shown a tremendous increase. (Source: Amaysim Financial disclosures Jun-16)

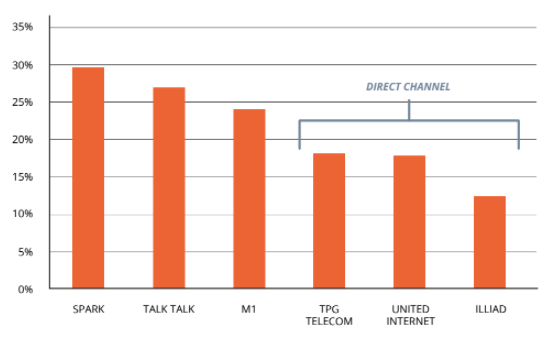

Most telcos are now actively pursuing digitisation as costs for customers transacting online are significantly lower than traditional telecom channels. They are driving a mobile centric digital experience which is further enhanced by using historical and real-time data to make intelligent product recommendations and simplify customer help options. However, not all telcos have jumped the online bandwagon. Spark NZ in its 2017 results disclosure has indicated that only 10% of its customers use the online channel. Analysis of indirect costs such as marketing, personnel and corporate costs suggests that online/call centre based operators (like Amaysim and TPG) have a cost structure of 12-18% of their total sales. This increases to mid-high 20s for full customer service operators like Spark. The table below indicates Indirect Operating cost ratios for a few Singapore, Australia and NZ based firms (excl. COGS and network expense). (Source: Analysis based on company disclosures Jun-16)

Turning The Care Model Upside Down

The traditional care model has customers waiting in long call queues, slogging through menus and talking to reps struggling to access all their information. This is now changing as telco operators are reinventing the care experience in many ways:

- Creating a pro-active self-serve experience. For example, Optus’ My Optus app not only lets you know your bill for the month, but also integrates insights around how much data you have used, the breakdown of which sites have used how much data etc. It even allows you to pay through the app in simple easy steps. There are also options to buy Optus Perks through the app. The app offers options for interactive chat with a customer care representative.

- Enabling an omni-channel care for experience and efficiency - many telecoms are gearing towards this. If a customer starts a technical troubleshooting call online and partway through decide to call live care, the history and context of the online interaction is passed to the rep and into the decision-making models that guide him or her.

- Using open source care in which customers can help resolve one another’s issues, leveraging machine learning to match customers with others who have had similar problems. Again, Telstra champions in this regard with a huge online community.

- Platinum Care: Telstra introduced the Platinum customer service a few years ago to look after customers ongoing technology leads. They pitch it as more than technical support but more about getting human help with the tech. For platinum customers, Telstra’s experts are available 24x7 to help customers get their technology connected, get support when they need it online, over the phone, at home or in store.

Changing The Face Of Call Centres

Telcos traditionally have had a heavy reliance on call centres to sell products as well as for managing customer care. Historically call centres used to be stationed in the country of service. However, the outsourcing model has seen most of Australian and NZ telcos moving to outsource from India and Philippines. The standard practice has been to outsource the less technical functions overseas and retain Tier 1 technical call centre staff who manage complex issues locally. Call centres are constantly moving up the value chain. Not only are they supporting technical issues, they are increasingly being used for more nuanced activities like business procurement, billing systems management, IT management, human resources management etc. iiNet in Australia sets a different example for technical support 24x7. It has its call centre staffs placed around the globe ranging from NZ to South Africa such that customers can get help whenever they need. The average cost of a call by geography (cents per call) as below:

Of course, this offshoring has come at the cost of compromising on quality as telcos have notoriously varied their mix in quality of onshore and offshore call centres.

Rapid adaptation of mobile technology and cloud communications

There has been a shift away from license based, on premise software. The increasing usage of Amazon web services and Mobile SIM management platforms like Jasper (CISCO) by many telcos including Telstra to host applications and platforms validates this. This is changing the way organisations provide customer service and support – allowing greater flexibility to ramp up capacity when call volumes increase, as well as engaging enterprise experts who are more empowered than agents to help with call resolution.

Increasing focus on speech analytics and call categorisation

Machines or programs are now identifying words or phrases in spoken language and natural speech to convert them into a machine-readable format. Call centres have been using interactive voice response (IVR) systems for a while now. They use speech recognition technology to allow customers to interact with the system by speaking instead of pushing buttons. However, beyond IVR systems, call centres have adopted other speech recognition applications such as call routing, speech-to-text, voice dialling and voice search to more efficiently handle incoming calls. There has also been a trend in outbound calling with IVR-based surveying.

Social Media

Sites such as Twitter and Facebook are being increasingly used to handle customer service. If you haven’t done it already, make a complaint directly to a company using their Twitter name or via their Facebook page. You’ll not only have the social media team interacting with you but will potentially have call centre agents communicating with you too. Call centres, like most media service providers, have been forced to offer multi-channel solutions.

The Rise Of Big Data In Customer Support

There has been increased marketing focus on customer engagement, customer satisfaction, and data analytics. With this increased focus on the level of customer care and striving for satisfaction call centres have improved the level of reporting on statistics and actionable insights from their call activity.

Internet of things and customer touch points

Telstra introduced the Smart Home automating and energy kit as well as the watch and monitor starter kit to their retail stores recently. These provide a system of connected smart devices all under the customer’s command. This is but a small step towards a much-enhanced customer service model. Disruptive data collection is allowing real time personalisation. Telcos are powering major venues to use sensor tracked foot traffic data to understand purchase activity and to optimise everything from store layouts to shop inventory to bathroom locations. Telcos are using identity based attribution and marketing optimisation to not only deliver ads but control the broader environment in which the ad is delivered. Those environments influence ad performance in subtle but important ways.

The Future Of Telco Customer Centricity

For all telcos that are facing becoming obsolete, the answer lies in focusing on customer and improving customer experience right through their journey, whether it be online; on social media; in the car stuck; at work; or in retail stores. The mantra is three fold:

- Understand your own customer base first - The easiest customers to reach are your own. Effective below the line communication can help keep your own customers engaged with you as you learn more about them. An essential part of this is engaging with customers in social blogs or forums and understanding their pain points.

- Enhance data driven analysis right across the organisation (from the front customer facing areas right to the commercial engine of the organisation) to understand where there is mutual value for the customer and the organisation. Focusing on this area is the key to enhanced customer satisfaction and reduced churns.

- Constantly improve customer facing areas of sales and care with the intention of surprising and delighting the customer. The most common complaint nowadays as most telcos move to a digital self-serve model is the long waiting times on the phone to reach a Customer centre executive. Increasing focus on speech analytics and call categorisation is the key to effectively managing customer expectations.

In a large country like Australia, network coverage is a huge pain point. Having detailed maps of network coverage for each region and communicating this effectively at point of sale to customer sets the right tone and prevents future regret from both parties. Last but not the least, organisations need to adopt a customer centric culture not only at the customer facing ends but also internally.

Infographic